Latest News Articles

Keeping you up to date with the latest Tax news.

Stay informed with our Monthly Newsletter

Sign up here:

CATEGORIES

- (50)Accounting & Financial Reporting

- (1)Accounting for Income Tax

- (1)Assessed losses

- (20)Blogs

- (1)Business Advisory

- (8)Capital Gains Tax

- (1)Capital Gains Tax - Individuals Tax

- (1)Capital Gains Tax Implications of Trusts

- (2)Case study: Home office expense

- (1)Case study: Travel allowances

- (1)Company Formations

- (136)Corporate Tax

- (12)Customs and Excise

- (2)Deceased Estate

- (1)Deductions Pre-trade and prepaid expenses

- (1)Deregistration

- (2)Employer and Employee (PAYE and UIF Specific)

- (1)Estate Duty

- (1)Events / Webinars

- (11)Faculty News

- (2)Farming

- (168)Individuals Tax

- (1)Input - Customs Duty

- (3)Interest

- (18)International Tax

- (1)Nature of the rights of beneficiaries

- (1)Notional input tax

- (9)Payroll

- (2)Practical Payroll

- (1)Professional Ethics

- (2)Provisional tax (Link with other Taxes)

- (4)SARS Issues

- (161)Tax Administration

- (2)Tax Administration Part 2B: Resolving Problems with SARS using the Tax Ombud

- (1)Tax Administration Part 3B Dispute Resolution - Objection and appeal

- (3)Tax Dispute Resolution

- (1)Tax Opinions

- (3)Tax Update

- (1)Tax implications of loans to trusts

- (1)Tax residence

- (1)Tax returns and payments

- (3)Transfer-Pricing

- (1)Trust Income / Gain Allocations

- (1)Trust types and income allocations

- (11)Trusts

- (86)VAT

- (3)VAT periods

- (1)Wear and tear allowances

- (14)Wills, Estates & Succession

- (1)Zero Rated

- (2)eFiling

- Show All

Latest News

How Long Does It Take to Become a Tax Practitioner...

- 13 June 2026

- Blogs

Discover the pathways, requirements, and timelines to become a registered tax practitioner in South...

Read More

Mastering VAT in South Africa: Your Guide to the B...

- 13 June 2026

- Blogs

Discover the best Value-Added Tax courses in South Africa to boost your accounting career.

Read More

Payroll and Tax Admin Courses: What You'll Learn

- 13 June 2026

- Blogs

Discover what you'll learn in payroll and tax admin courses, including PAYE, payroll compliance, SAR...

Read More

What Does a Tax Technician Actually Do?

- 11 June 2026

- Blogs

Discover the responsibilities, career opportunities, skills, and qualifications needed to become a t...

Read More

Tax Courses vs Accounting Courses: What’s the Diff...

- 21 May 2026

- Accounting & Financial Reporting

Discover the difference between tax and accounting courses in South Africa. Learn how tax profession...

Read More

Careers You Can Start with a Taxation Certificate

- 22 May 2026

- Blogs

Explore careers you can start with a taxation certificate in South Africa, from tax practitioner and...

Read More

Entry-Level Tax Courses You Can Start Without a De...

- 22 May 2026

- Blogs

Starting a career in tax does not require a university degree. In fact, many professionals enter the...

Read More

What Are the Best Tax Courses in South Africa?

- 21 May 2026

- Blogs

Discover the best tax courses in South Africa, including tax practitioner training, VAT, payroll, an...

Read More

I Just Finished Matric - What Are My Options in Ta...

- 24 May 2026

- Blogs

If you are interested in finance, problem-solving, or business, tax is one of the most overlooked bu...

Read More

The Difference Between a Tax Technician and a Tax...

- 24 May 2026

- Blogs

For anyone considering a career in tax, one of the most common points of confusion is the difference...

Read More

Getting your customs classification wrong may be a...

- 25 May 2026

- Customs and Excise

With 1,228 tariff headings in South Africa, getting your classification wrong can lead to heavy pena...

Read More

Wealth Does Not Last: Why Estate Planning Strategi...

- 14 May 2026

- Wills, Estates & Succession

Wealth rarely survives beyond a few generations—but it doesn’t have to be that way. This article exp...

Read More

Stealth Taxes: Customs and Excise

- 29 April 2026

- Customs and Excise

Customs and excise duty is often viewed as a mysterious tax which somehow finds its way into the pri...

Read More

Tax Faculty vs Unisa: Choosing the Right Tax Educa...

- 22 April 2026

- Blogs

Choosing the correct educational path in taxation can drastically shape your career trajectory. As y...

Read More

Objections That Work: Drafting Technical Objection...

- 08 April 2026

- Tax Administration

Stop treating tax objections as procedural speed bumps. This article explains why precision - not ou...

Read More

Is VAT eating away at your cash flows?

- 02 April 2026

- VAT

VAT is often viewed as a flow-through tax which is only relevant to the final consumer. While this m...

Read More

Mastering ADR and Settlements: A Procedural Guide...

- 25 March 2026

- Tax Administration

Master ADR and settlements with this procedural guide. Learn to navigate SARS's confidential, withou...

Read More

Navigating the New Era of Trust Compliance in Sout...

- 24 March 2026

- Trusts

Stay ahead of the "SARS enforcement crackdown" with this essential guide to trust compliance in 2026...

Read More

Navigating SARS Administrative Fairness: A Guide f...

- 10 March 2026

- Tax Administration

The power gap between SARS and taxpayers is widening. From eFiling profile hijacking to unexplained...

Read More

The AI Risk Trilogy: Essential Ethics and Risk Man...

- 16 March 2026

- Professional Ethics

This is a timely and well-structured breakdown of a critical shift in the South African professional...

Read More

Navigating Tax Disputes: A Guide to SARS Objection...

- 17 March 2026

- Tax Administration

In an era of increasing scrutiny, navigating tax disagreements requires precision. This guide breaks...

Read More

Protecting Taxpayers’ Rights: Why Every Tax Practi...

- 30 March 2026

- Tax Administration

Master the Tax Court’s "disputes within a dispute." Join our specialized webinar to unpack applicati...

Read More

New VAT registration rules – What you need to know

- 30 March 2026

- VAT

This article explores the intricate challenges currently impacting the industry. It highlights the n...

Read More

The Power of Continuous Tax Education for South Af...

- 25 February 2026

- Individuals Tax

In the ever-evolving world of taxation, continuous education is crucial for accountants and tax prac...

Read More

Individuals Tax News

The Power of Continuous Tax Education for South Af...

- 25 February 2026

- Individuals Tax

In the ever-evolving world of taxation, continuous education is crucial for accountants and tax prac...

Read More

From Zero to Tax Hero: Understanding the Basics of...

- 21 February 2026

- Individuals Tax

This guide will simplify taxation basics, equipping you with a strong foundation to confidently begi...

Read More

Provisional Tax: Practical Guidance to Avoid Penal...

- 14 January 2026

- Individuals Tax

This article unpacks provisional tax, who it applies to, and why reasonable estimates are key to avo...

Read More

Corporate Tax News

Navigating the enhanced section 11D R&D incentive

- 21 October 2025

- Corporate Tax

The Section 11D R&D tax incentive, outlining recent legislative changes, eligibility criteria, quali...

Read More

Vehicle Fringe Benefits in a CC: South African Tax...

- 21 July 2025

- Corporate Tax

Two Close Corporation (CC) members use vehicles registered in the CC’s name solely for private purpo...

Read More

Deferred Tax: The Quiet Complexity Lurking in Fina...

- 16 July 2025

- Corporate Tax

Deferred tax is more than an accounting issue—it impacts financial clarity and tax compliance. This...

Read More

VAT periods News

Getting out what you put in…A recap on the deducti...

- 19 December 2019

- VAT periods

Author: Varusha Moodaley

Read More

Further clarification on the VAT registration of n...

- 19 December 2019

- VAT periods

Author: Jerome Brink

Read More

Contingency Fees: VAT inclusive or exclusive?

- 27 May 2021

- VAT periods

Author: Gerhard Badenhorst

Read More

Tax returns and payments News

Weekly transfer pricing roundup – 19 June 2017

- 19 June 2017

- Tax returns and payments

Author: Marcus

Read More

Deregistration News

Deregistration as a VAT Vendor

- 27 May 2020

- Deregistration

A sole proprietor performs services for clients abroad. More than 90% of the taxpayer’s revenue is d...

Read More

Zero Rated News

[FAQ] Is the sale of borehole water a zero-rated s...

- 03 August 2020

- Zero Rated

Client “A” is a farmer who is a registered VAT vendor. His neighbour (Client “B”) is a poultry farme...

Read More

Notional input tax News

Value-added tax & transfer duty: Clarity or confus...

- 22 June 2020

- Notional input tax

Where fixed property is purchased by a VAT vendor from a non-vendor, transfer duty is payable thereo...

Read More

Input - Customs Duty News

VAT on imported services payable by non-registered...

- 05 June 2020

- Input - Customs Duty

On 1 June 2020, the South African Revenue Service (SARS) issued an external guide titled ‘Manage Dec...

Read More

Farming News

Welcome clarity on the taxation of farmers in Sout...

- 07 October 2022

- Farming

Welcome clarity on the taxation of farmers in South Africa?

Read More

Farmers claiming diesel rebate

- 17 February 2020

- Farming

The Supreme Court of Appeal recently overturned a decision by the High Court. The impact of the deci...

Read More

Capital Gains Tax - Individuals Tax News

[FAQ] The tax implication when cryptocurrency is s...

- 23 April 2021

- Capital Gains Tax - Individuals Tax

It is stated that income on cryptocurrency that was mined will be taxed when income is received/accr...

Read More

Practical Payroll News

Payment holiday for Skills Development Levy contri...

- 26 June 2020

- Practical Payroll

The COVID-19 outbreak together with extended lockdown continues to have a negative impact on the cas...

Read More

[FAQ] EMP501 Reconciliations

- 12 June 2020

- Practical Payroll

The taxpayer works as a tax practitioner at a company where they submit between 150 to 200 EMP501 re...

Read More

Employer and Employee (PAYE and UIF Specific) News

Employees’ Tax

- 22 March 2022

- Employer and Employee (PAYE and UIF Specific)

The Guide for Employers in respect of Employees Tax for 2023 has been updated to include the new tab...

Read More

[FAQ] Should benefits received from the South Afri...

- 17 November 2020

- Employer and Employee (PAYE and UIF Specific)

Should benefits received from SAFT be included or excluded from the IRP5 and will these benefits rec...

Read More

International Tax News

Navigating Withholding Tax on Cross-Border Service...

- 16 July 2025

- International Tax

Guidance for South African service providers on claiming withholding tax relief for cross-border tra...

Read More

Seafarer Tax Exemption: Navigating Section 10(1)(o...

- 01 June 2025

- International Tax

A brief analysis of whether South Africans working on yachts abroad qualify for the seafarer tax exe...

Read More

Tax Considerations for South African Companies Act...

- 11 June 2025

- International Tax

An overview of the tax, exchange control, and legal risks when a South African company acts as an Em...

Read More

Tax Administration News

Objections That Work: Drafting Technical Objection...

- 08 April 2026

- Tax Administration

Stop treating tax objections as procedural speed bumps. This article explains why precision - not ou...

Read More

Mastering ADR and Settlements: A Procedural Guide...

- 25 March 2026

- Tax Administration

Master ADR and settlements with this procedural guide. Learn to navigate SARS's confidential, withou...

Read More

Navigating SARS Administrative Fairness: A Guide f...

- 10 March 2026

- Tax Administration

The power gap between SARS and taxpayers is widening. From eFiling profile hijacking to unexplained...

Read More

VAT News

Is VAT eating away at your cash flows?

- 02 April 2026

- VAT

VAT is often viewed as a flow-through tax which is only relevant to the final consumer. While this m...

Read More

New VAT registration rules – What you need to know

- 30 March 2026

- VAT

This article explores the intricate challenges currently impacting the industry. It highlights the n...

Read More

Are You Confident That You Will Survive a SARS VAT...

- 16 February 2026

- VAT

A practical look at preparing for a SARS VAT audit, avoiding common pitfalls, and managing disputes...

Read More

Payroll News

Payroll Considerations Managing New Employee Costs

- 09 July 2024

- Payroll

A client hired a new employee with a monthly cost to the company of R20000, without specifying if co...

Read More

[FAQ] Retrospective application for a severance ta...

- 29 July 2021

- Payroll

An employee received a lump sum when he left which was seen as a bonus payment. The employee left du...

Read More

[FAQ] Employment Tax Incentive and connected perso...

- 23 June 2021

- Payroll

Would a taxpayer be eligible to register his son under the business ETI or is he considered to be a...

Read More

Transfer-Pricing News

The Arm’s Length Principle: Foundation of Transfer...

- 27 November 2025

- Transfer-Pricing

This article explains the arm’s length principle, the foundation of South Africa’s transfer pricing...

Read More

Transfer Pricing in South Africa: An Arm’s Length...

- 20 September 2024

- Transfer-Pricing

straightforward and consistent with established transfer pricing principles. The court sharply criti...

Read More

Transfer Pricing has Finally Washed up on South Af...

- 25 March 2024

- Transfer-Pricing

With increasing economic globalisation, revenue authorities around the world continue to shift their...

Read More

Wills, Estates & Succession News

Wealth Does Not Last: Why Estate Planning Strategi...

- 14 May 2026

- Wills, Estates & Succession

Wealth rarely survives beyond a few generations—but it doesn’t have to be that way. This article exp...

Read More

Estate Duty Planning: Utilising the General Deduct...

- 15 July 2025

- Wills, Estates & Succession

Overview of estate duty deductions and how a surviving spouse can use an unused basic amount from th...

Read More

Navigating Tax Consequences for Family Trusts: Int...

- 18 June 2025

- Wills, Estates & Succession

A brief analysis of tax issues in South African family trusts, covering interest income, trustee wit...

Read More

Customs and Excise News

Getting your customs classification wrong may be a...

- 25 May 2026

- Customs and Excise

With 1,228 tariff headings in South Africa, getting your classification wrong can lead to heavy pena...

Read More

Stealth Taxes: Customs and Excise

- 29 April 2026

- Customs and Excise

Customs and excise duty is often viewed as a mysterious tax which somehow finds its way into the pri...

Read More

VAT Implications of Exporter of Record Designation...

- 14 April 2025

- Customs and Excise

This article analyses the correct designation of the Exporter of Record on the SAD500 form for indir...

Read More

Tax Update News

IT3(d) Third Party Data FAQs

- 28 May 2024

- Tax Update

IT3(d) onboarding, testing and live submissions will remain open for the duration of the submission...

Read More

2022 MTBPS: Generally good news, limited tax chang...

- 01 November 2022

- Tax Update

2022 MTBPS: Generally good news, limited tax changes

Read More

The 2020 Tax Amendments

- 17 December 2020

- Tax Update

The National Treasury recently published a number of bills that contain the amendments to the tax la...

Read More

Tax Opinions News

Bad Debt Deductions for Bodies Corporate: Income T...

- 15 July 2025

- Tax Opinions

A brief analysis of when bad debts are tax-deductible for a body corporate, based on exempt vs taxab...

Read More

Tax Dispute Resolution News

Yes, You Really Can Mess Up A SARS Objection

- 07 February 2025

- Tax Dispute Resolution

The Western Cape Tax Court case DR X and Dr X Inc v CSARS highlights the problem of vague and unsupp...

Read More

Revenue Augmentation: Low Hanging Fruit

- 14 June 2024

- Tax Dispute Resolution

In an apparent effort to win the war against non-compliance, it seems SARS has taken to augmenting t...

Read More

Dispute resolution - Is it time to settle?

- 12 August 2020

- Tax Dispute Resolution

The settlement of a tax dispute is available to taxpayers in respect of which an assessment has been...

Read More

Interest News

General rules regarding interest deductibility

- 17 August 2020

- Interest

In the current environment where there is a huge amount of debt being incurred by taxpayers it is us...

Read More

BGR 53 - Rules for the taxation of interest payabl...

- 22 June 2020

- Interest

This BGR sets out the rules to avoid double taxation when a deemed accrual of interest occurs under...

Read More

Updated Table of interest rates: Table 3 – Rates a...

- 27 January 2020

- Interest

Where a loan is obtained by an employee from his or her employer in terms of which no interest is pa...

Read More

Deductions Pre-trade and prepaid expenses News

Did the SCA get this right?

- 06 July 2020

- Deductions Pre-trade and prepaid expenses

Section 23H of the Income Tax Act is a provision that is designed to spread prepayments made by taxp...

Read More

Assessed losses News

Proposed changes to Assessed loss provision

- 15 September 2021

- Assessed losses

The 2021 Draft Laws Amendment Bill that was released in July 2021, has proposals to change section 2...

Read More

Wear and tear allowances News

BGR 7 - Wear-and-tear or depreciation allowance

- 15 February 2021

- Wear and tear allowances

This BGR reproduces the parts of Interpretation Note 47 (Issue 5) “Wear-and-Tear or Depreciation All...

Read More

Capital Gains Tax News

Sale of Share Options on Resignation

- 12 January 2024

- Capital Gains Tax

Payout classification for employees leaving after receiving company shares depends on factors like a...

Read More

[FAQ] The tax implication when shares are sold for...

- 26 August 2021

- Capital Gains Tax

A Trust owns 100% of the ordinary shares in a company and charges R20 million to a potential purchas...

Read More

[FAQ] Capital Gains Tax on the sale of shares wher...

- 12 August 2021

- Capital Gains Tax

A taxpayer is a director who wants to sell her shares to the remaining directors. The shares have a...

Read More

Trust types and income allocations News

Guide to the Taxation of Special Trusts (Issue 3)

- 10 September 2020

- Trust types and income allocations

The purpose of this guide is to assist users in gaining a more in-depth understanding of the taxatio...

Read More

Trust Income / Gain Allocations News

BPR 350 – Vesting of a capital gain in a trust ben...

- 14 September 2020

- Trust Income / Gain Allocations

This ruling determines the tax consequences of the vesting of a capital gain in a beneficiary, where...

Read More

Nature of the rights of beneficiaries News

The tax implications of medical expenses paid by a...

- 21 May 2020

- Nature of the rights of beneficiaries

The trust, special trust or otherwise, cannot make a deduction of the medical expenditure incurred o...

Read More

Tax implications of loans to trusts News

Amendment to section 7C: Beware of preference divi...

- 19 November 2020

- Tax implications of loans to trusts

With the introduction of section 7C, the interest saving arising on interest-free or low interest ra...

Read More

Capital Gains Tax Implications of Trusts News

Tax implications of terminating a trust

- 19 October 2020

- Capital Gains Tax Implications of Trusts

A trust is terminated by the Master after all the trust property was vested and distributed to the b...

Read More

Provisional tax (Link with other Taxes) News

[FAQ] How do you submit a Third Prov Tax return an...

- 22 August 2023

- Provisional tax (Link with other Taxes)

[FAQ] How do you submit a Third Prov Tax return and what penalties are payable if any?

Read More

[FAQ] Provisional tax when the financial year-end...

- 19 August 2021

- Provisional tax (Link with other Taxes)

A company changed its financial year-end from February to June. The change was made on 13 March 2021...

Read More

Deceased Estate News

How should a Deceased Estate be administered?

- 20 August 2020

- Deceased Estate

The administration of a deceased estate entails a regulatory process overseen by the Master of the H...

Read More

Estate Duty News

Company Formations News

BGR 54 - Unbundling of unlisted company: Impact of...

- 22 June 2020

- Company Formations

This BGR provides clarity on what constitutes an unbundling transaction when an unbundling company h...

Read More

Tax residence News

New proposal for required documents when ceasing t...

- 30 September 2021

- Tax residence

There has been a proposal that has been issued with new document requirements for taxpayers who wish...

Read More

Accounting for Income Tax News

Base Cost For Shares

- 16 February 2024

- Accounting for Income Tax

A trust adjusts share values annually but base cost remains R500 despite fair value changes under th...

Read More

Tax Administration Part 2B: Resolving Problems with SARS using the Tax Ombud News

[FAQ] What remedies are available to a taxpayer as...

- 24 July 2020

- Tax Administration Part 2B: Resolving Problems with SARS using the Tax Ombud

A taxpayer has lodged and objection with SARS. The objection was accepted, but SARS did not comply w...

Read More

[FAQ] Can the Tax Ombud assist with issues regardi...

- 22 July 2020

- Tax Administration Part 2B: Resolving Problems with SARS using the Tax Ombud

VAT returns submitted and paid through eFiling reflect on the taxpayer's work page. However, the ret...

Read More

Trusts News

Navigating the New Era of Trust Compliance in Sout...

- 24 March 2026

- Trusts

Stay ahead of the "SARS enforcement crackdown" with this essential guide to trust compliance in 2026...

Read More

Capital Gains Tax Risks for Trusts: The Dangers of...

- 10 June 2025

- Trusts

An analysis of the tax risks trusts face when relying on incorrect IT3(c) base costs, highlighting c...

Read More

Tax Treatment of Rental Income Distribution via Tr...

- 17 May 2025

- Trusts

The question examines the South African tax implications of distributing rental income through a tru...

Read More

Accounting & Financial Reporting News

Tax Courses vs Accounting Courses: What’s the Diff...

- 21 May 2026

- Accounting & Financial Reporting

Discover the difference between tax and accounting courses in South Africa. Learn how tax profession...

Read More

Tax Implications of Legal Fees Incurred as Part o...

- 07 April 2025

- Accounting & Financial Reporting

A brief analysis of the tax treatment of legal fees within management services, focusing on deductib...

Read More

The Future of Tax: How Technology is Reshaping the...

- 22 April 2025

- Accounting & Financial Reporting

This article explores how emerging technologies like AI, automation, and cloud-based solutions are t...

Read More

Events / Webinars News

ChatGPT and AI for Accountants

- 03 May 2024

- Events / Webinars

ChatGPT – it’s the latest buzzword, and for good reason. This powerful new tool has the potential to...

Read More

Tax Administration Part 3B Dispute Resolution - Objection and appeal News

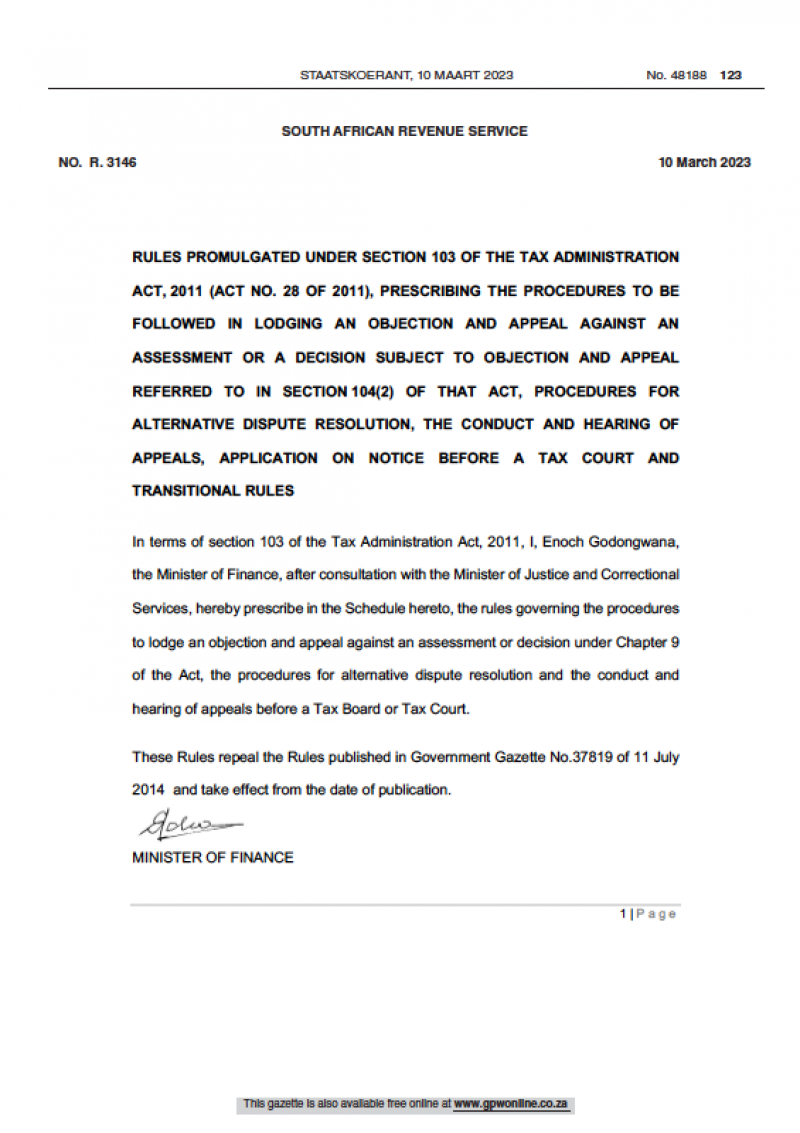

New Tax Dispute Resolution Rules (Effective 10 Mar...

- 11 March 2023

- Tax Administration Part 3B Dispute Resolution - Objection and appeal

The Minister of Finance approved new dispute resolution rules under the Tax Administration Act, 2011...

Read More

Case study: Travel allowances News

[FAQ] What is the correct tax treatment of employe...

- 28 August 2023

- Case study: Travel allowances

[FAQ] What is the correct tax treatment of employee travel allowances?

Read More

Case study: Home office expense News

[FAQ] Home office expense regarding solar installa...

- 22 August 2023

- Case study: Home office expense

[FAQ] Home office expense regarding solar installation

Read More

[FAQ] Home office expenses

- 21 October 2020

- Case study: Home office expense

A company has staff that have been working from home during COVID19. In total, there are 3 working d...

Read More

Faculty News News

What is the SAICA Accounting Technician SA (AT(SA)...

- 07 August 2025

- Faculty News

The SAICA AT(SA) designation certifies accounting technicians holding the Certificate in Accounting...

Read More

Big Tax Hikes Coming for Businesses in South Afric...

- 04 December 2024

- Faculty News

Carbon taxes in South Africa are set to rise by over 140% by 2030.

Read More

The Tax Faculty Accredited by SAICA to Offer Accou...

- 10 June 2024

- Faculty News

The South African Institute of Chartered Accountants on Monday 3 June 2024 announced the accreditati...

Read More

Blogs News

How Long Does It Take to Become a Tax Practitioner...

- 13 June 2026

- Blogs

Discover the pathways, requirements, and timelines to become a registered tax practitioner in South...

Read More

Mastering VAT in South Africa: Your Guide to the B...

- 13 June 2026

- Blogs

Discover the best Value-Added Tax courses in South Africa to boost your accounting career.

Read More

Payroll and Tax Admin Courses: What You'll Learn

- 13 June 2026

- Blogs

Discover what you'll learn in payroll and tax admin courses, including PAYE, payroll compliance, SAR...

Read More

SARS Issues News

SARS Giveth and SARS Taketh Away

- 25 March 2024

- SARS Issues

The alarmingly high unemployment rate in South Africa has given rise to several tax incentives for e...

Read More

SARS and Tax Court Closing Dates

- 08 January 2024

- SARS Issues

SARS excludes December 16th to January 15th from "business days" as per TAA Section 1, impacting the...

Read More

SARS Clarifying Trust Income Tax Return Requiremen...

- 31 August 2023

- SARS Issues

The purpose of this notice is to address these common issues, which may have been communicated durin...

Read More

eFiling News

Navigating eFiling: Operational and Processing Ess...

- 30 July 2025

- eFiling

This article outlines essential steps for navigating SARS eFiling during the 2025 Filing Season, inc...

Read More

eFiling Taxpayer Profile Hijackings on the Increas...

- 11 June 2024

- eFiling

You can be held liable for whatever a hacker manages to siphon from Sars in your name.

Read More

Business Advisory News

Address Unforeseen Threats Undermining Business St...

- 13 September 2024

- Business Advisory

Risk is an inherent part of running any business, yet many business owners overlook the importance...

Read More

Professional Ethics News

The AI Risk Trilogy: Essential Ethics and Risk Man...

- 16 March 2026

- Professional Ethics

This is a timely and well-structured breakdown of a critical shift in the South African professional...

Read More